4 / 74

4 / 74

High-Tech & Technology -

DUN’S

100

|

2016/17

4

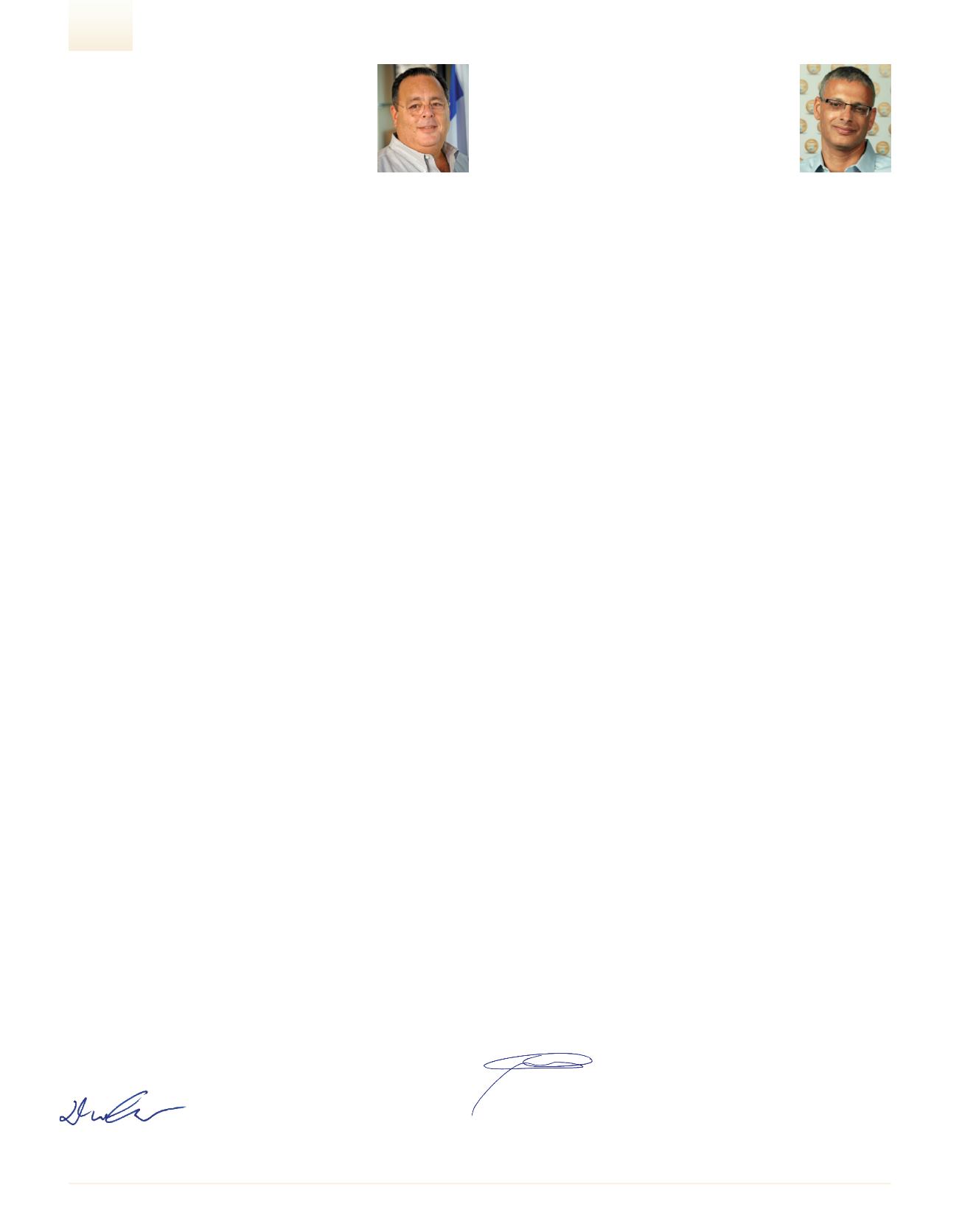

Eitan Madmon

CEO Globes

Dear readers,

The human race is facing a great, multi-dimensional

challenge with vast implications. An entire army of technological developers

is working, operating and generating tools, services and strategies which

are about to change our way of life as we know it.

The rate of change is inconceivable, and imagination becomes a reality, at

an astounding speed. All of the science fiction movies from the early 70s to

the early 90s are already a reality in our everyday lives. Most of our children

already breathe and live a world which is completely different from the world

we’ve known. And the most amazing thing is that the rate of change keeps

accelerating every year.

Is the world really going to create, through human beings, a different, alien

reality, such as the reality which is depicted in films such as “The Matrix”?

Apparently so. And very clearly. The way we live would be shaped more and

more by corporations, not governments. Nowadays we can already analyze

and make quite a clear prediction, that the future global superpowers won’t

be countries, but rather corporations.

Two prominent examples of this, with ever-growing power, are Google and

Facebook. Beyond the major familiar core products of each company, a

search engine and a social network, they allocate enormous resources and

invest in super-projects in a way that would provide them with control over

the minds, the intellects and the actions of each and every one of us.

Facebook is currently racing to create a super-platform, through which it

would affect information and reality as we shall consume them in the future.

This, with the pretention of reaching an almost perfect control of the content

we consume. Google is in the midst of a great effort to generate tools and

services which will manage all of our lives in every given moment – from

the autonomous car to artificial intelligence.

Whether this is good or bad should be left for Historians and Anthropologists

to decide. But this seems to be the reality which would accompany us in

the next decade or two. One thing is already clear today – whoever wishes

to be part of the new game must be a person with autonomous initiative

and drive, and not someone who is driven by others.

The Israeli High-Tech Industry certainly has a presence on this playing field.

It is true that we don’t have our own Google or Facebook, but we do have

various components, small and significant, which would be a part of and

would comprise the technology puzzle of this brave new world. We have

extraordinary innovation which interests the whole world. Prominent multi-

national companies maintain development centers in Israel, while simulta-

neously reviewing and identifying potential investments.

This is certainly a commendation for the Israeli High-Tech Industry. This

advantage must be preserved, strengthened, encouraged and supported.

The potential is clear and proven. How it would be utilized is greatly depen-

dent on the moves and the decisions that would be made here.

This special edition yearbook presents a miniscule, if important, part of the

potential of the industry in Israel.

I wish you a pleasant, enjoyable reading.

Eitan Madmon

CEO, Globes

Doron Cohen

Chairman & CEO Dun & Bradstreet Israel

2016 was another solid growth year in the perpetually ma-

turing Israeli high-tech industry. The industry is producing

more growth-focused companies with long-term business

strategies, and is now taking a more significant share of the

pie in the acquisition of Israeli startup companies.

Currently, from the data we collected, about 6,650 high-tech companies operate

in Israel, of which about 4,750 (approx. 71.5% of all high-tech companies) are

startups in various stages of the VC cycle. About 3,650 startups (approx. 77% of

the all startups) have raised capital at least once from an external source, such

as government funding, angels and VC funds .

2015 saw a number of large private fundraising rounds, amounting to tens of

millions of dollars each, for growth-stage companies that generate substantial

business activity and jobs. In the past, many of these companies would have

opted for an exit at this stage, rather than a growth round; the change repre-

sents a significantly positive shift in the industry. We see a very large number of

serial entrepreneurs in the market; more than one quarter of the entrepreneurs

of currently active startups are serial entrepreneurs, and their contribution to

the industry is invaluable. Their experience is material to the maturation of the

industry enabling better survival rates, more, and larger, capital rounds, and the

establishment of longer-term companies.

We are clearly seeing the results of this trend, as more and more Israeli tech

startups are taking the significant steps towards becoming sustainable growth

companies. Currently 385 companies in the industry are large companies with

more than 100 employees (approx. 6% of all companies), representing a 29%

increase over the past six years. Another indicator which we view as significant

towards the maturity of the industry, is the increasing bootstrapping period of

many startups. This happens even though there is a relative high availability of

capital for fundraising. This situation, which speaks directly to the positive impact

serial entrepreneurs are having on the industry, requires entrepreneurs to man-

age the startup during the initial stages at a lean cost structure, without burning

excessive funds, with the objective being to place the company in a stronger

position to execute on a long term growth strategy.

The Israeli high-tech industry is, as it always has been, a leader in identifying and

acting on new ideas in growing fields. The growth in the FinTech industry, one

of the fastest growing global sectors, saw Israel FinTech startups raise the most

capital, globally, over the past two years, with approximately $500M raised per

year.The Cyber field, too, saw significant funding into Israeli startups amounting to

about $500M in 2016. Some reports indicate that asmuch of 15%of 2016 global

cyber venture investment was directed at Israeli companies. This trend further

cements Israel’s position as a leader in the techworld, consistently strengthening

the reputation of the local industry across the globe.

The lack of qualified local human resources remains a significant challenge for

the industry, bringing about amaterial barrier to its development.The demand for

high-tech employees has increased, with costs following suit. This is true mainly

for thosewhoworkon the server-side software development and in IT.The heavier

demand for human capital ismainly fromstartups and growth companies; mature

companies continue to ebb and flow, streamlining their workforce in recent years,

with large layoffs, for example in the multinationals - HPE, Intel, Cisco and Frees-

cale Semiconductors, and in large Israeli companies such as Nice andVerint. The

Israeli high-tech industrymust continue toworkthrough these barriers promoting

a supportive eco-system, in order to enable its continued growth.

Looking forward to 2017, we will continue to provide unique access and insight

into the Israeli high-tech universe through this yearbook edition of Dun’s 100.

The yearbookprovides a glimpse into current activities and trends in the industry,

also presenting various rankings, reviews, outlooks, articles and opinions, aswell

as the profiles of the industry’s leaders and startups.

We lookforward to the continued prosperity of the Israeli High-Tech industry, which

is one of the main and important growth accelerators of the Israeli economy.

Sincerely,

Doron Cohen

Chairman & CEO, Dun & Bradstreet Israel