8 / 74

8 / 74

High-Tech & Technology -

DUN’S

100

|

2016/17

8

High-Tech Industry Snapshot

(Continues)

a later stage with a higher valuation. The num-

ber of bootstrapping companies amounted to

approx. 1,100, roughly 23% of all start-ups in

the local industry.

A More Mature Industry

A distinct trends in the local industry, over the

past few years, is the increase in the involve-

ment of more experienced entrepreneurs.

In 2010, the number of entrepreneurs who

founded and managed at least two start-up

companies was 16% of the total number of en-

trepreneurs in that year. In 2016, the number

of entrepreneurs who founded and managed

at least two start-up companies increased to

27%. The entrepreneurs’ experience is of a

critical importance to the development of the

High-Tech industry in Israel. Experienced en-

trepreneurs build companies for longer terms,

over the VC cycle. They provide better surviv-

ability and larger extents of fundraising and

they grow more mature companies. There are

more entrepreneurs with personal funds who

can build more mature companies.

The High-Tech Industry’s 10 Leading Cities

One of the catalysts of the High-Tech industry

is the eco-system in which it operates, wheth-

er if it consists of access to investors, to the

academy or to human capital. Approx. 62% of

all tech companies operate In the 10 leading

cities (by no. of tech companies), with Tel-Aviv

leading the list by a large gap, with about 28%

of tech companies. The tech companies in the

10 leading cities raised approx. 80% of the

total industry funding in 2016. The tech com-

panies in Tel-Aviv raised roughly 42% of the

industry’s total funding in 2016. The leading

sectors in the 10 leading cities are Internet,

IT and Enterprise Software and Life Sciences.

The contribution for creating the eco-system

in these cities may also come from attracting

mature tech companies to the city.

The Main Challenge – A Lack of Human

Capital

The lack of skilled human capital, particularly in

the software and the internet sectors, continues

to be the largest challenge of the local industry

- The average annual growth rate of High-tech

jobs in the past three years amounted to approx.

9,000 jobs per year, while the potential annual

growth amounted to approx. 13,000 new jobs.

The demand for human capital comes mainly

from the “roots” – from start-ups and growing

companies, while mature companies have been

streamlining their human resources in recent

years, with large layoffs.

We must reduce the human capital supply-

demand gap in the local industry, through

governmental direction for increasing the num-

ber of high-school graduates who completed the

core studies required for higher technological

education, such as 5 units of Mathematics and

Physics and Chemistry.

80

70

60

50

40

30

20

10

0

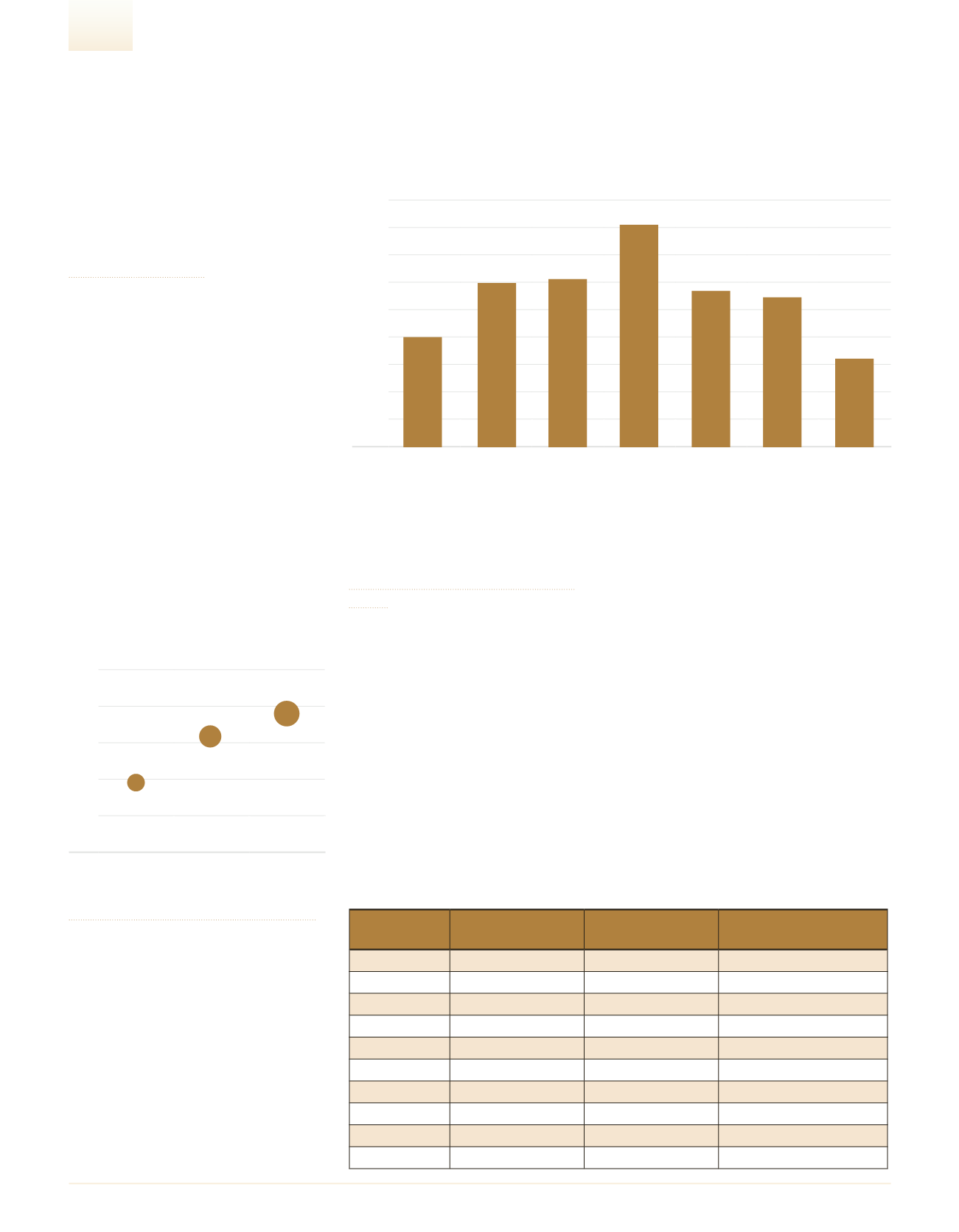

Semiconductors

Miscellaneous

Technologies

Life Sciences

IT & Enterprise

Sfotware

Internet

Communications

Cleantech

Leading Companies Distribution by Line of Business

40

60

61

57

54

32

81

400

+6%

350

+4.2% YTY

300

250

200

2016

2015

2010

High-Tech Companies with Over 100

Employees

City

% of the High-Tech

Industry

Number of High-Tech

Companies

Main Line of Business

Tel Aviv

27.61%

1,836

Internet

Herzliya

6.71%

446

IT & Enterprise Software

Jerusalem

5.07%

337

Life Sciences

Haifa

4.36%

290

Life Sciences

Ramat Gan

4.35%

289

Internet

Petah Tikva

4.02%

267

IT & Enterprise Software

Ra’anana

3.32%

221

Internet

Netanya

2.66%

177

Life Sciences

Kfar Saba

2.15%

143

IT & Enterprise Software

Rehovot

2.08%

138

Life Sciences

The High-Tech Industry`s 10 Leading Cities