27 / 730

27 / 730

Underwriting – Raising Funds and Offerings

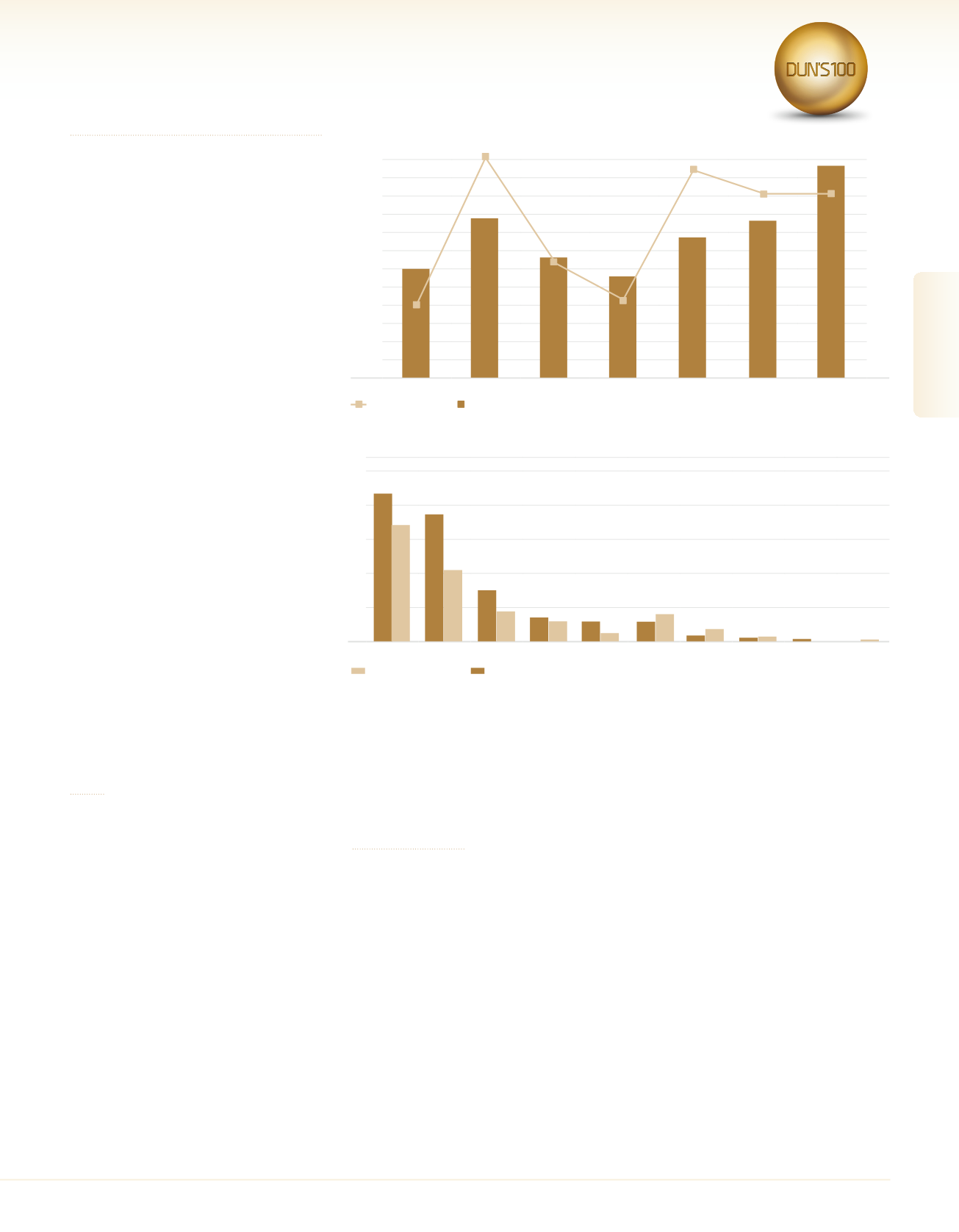

In 2015, 252 public offering were conducted

(bonds + shares) raising an overall amount of

about NIS 58 billion, compared with 252 offer-

ings in 2014 when an overall amount of about

NIS 44 billion was raised.

The total bonds raised in 2015, in public offering,

amounted to about NIS55 billion (179 offerings),

which represented a rise of about 39.5% com-

pared with 2014 (in which about NIS 39 billion

was raised). The total amount of bonds raised in

2015 represented about 94% of the total funds

raised during the year (compared with about 89%

in 2014).

Total capital raised (shares) in 2015, in public

offerings, amounted to about NIS 3.4 billion (73

offerings), representing a decline of about 28%

compared with 2014 (in which about NIS 4.7 bil-

lion was raised).

An analysis of the funds raised according to sec-

tors finds that the real estate and construction

sector raised about NIS21.7 billion in 2015 (com-

pared with about NIS 17.6 billion in 2014). In

terms of the number of offerings, it can be seen

that the real estate and construction sector led in

2015 with 114 offerings as well as in 2014 with

124 offerings.

In terms of the amount of funds raised, the indus-

try in second place in 2014-2015was the banking

sector. In 2015, this sector raised about NIS 18.3

billion (compared with about NIS 11 billion in

2014). In terms of the number of offerings, the

sector in second place in 2014-2015 was the

medical technology industry with 36 offerings in

2015 (compared with 29 offerings in 2014).

Banks

In 2015, Israel's five largest banks (Hapoalim,

Leumi, Mizrahi-Tefahot, Discount and First Inter-

national) reported net profit of NIS 8.2 billion,

an increase of 28% compared to 2014 (NIS 6.4

billion in 2014 and NIS 6.9 billion in 2013). The

increase in profit resulted primarily from weaker

results that Leumi and Discount had reported in

2014 – Leumi was required to set aside about

NIS 1 billion for an investigation by the U.S au-

thorities. In addition, Bank Leumi reported a one-

time income of about NIS 1 billion in 2015 from

realizing assets, a measure which increased its

profit. Total fees collected by the five big banks

amounted to NIS 14.8 billion (compared with NIS

15 billion in 2014). Total income from interest at

the five big banks amounted to about NIS 24.5

billion (similar to 2014). The five large banks cre-

ated return on equity (the ratio between net profit

and equity) of about 8.45% (comparedwith about

7% in 2014 and about 8.3% in 2013). Along

with the challenge of maintaining profitability,

the banks were also forced to cope with negative

influences such as a low interest environment as

well as the need to meet regulatory capital goals

(lowering ratio to leveraging, improving liquidity

ratios, improving core capital adequacy ratios,

and more).

Investment Houses

The investment houses sector in Israel has un-

dergone major changes in recent years, both in

regulatory and competitive terms. On the one

hand, the amount of assets managed has risen,

but at the same time so have the regulatory

requirements, and these have weighed on the

investment houses. In 2015, the sector under-

went amarketing transformation that focused on

the private customer (the household consumer),

while in the past the main marketing efforts by

investment houses concentrated on the media-

tors working for the private customer (insurance

agents, banks' investment consultants, etc.). The

Investment houses decided to directly approach

private customers after seeking new sources of

growth and profit and they understood that ap-

proaching customers directly can help them sell

additional financial products. In addition, private

customers are currently aware andmore involved

in the financial sector and consequently the in-

vestment houses are obliged to provide themwith

more information. Psagot Investment House's

position at the top of the rankings remains firm

and the company continues to lead the invest-

ment house rankings for the past eighth year. The

Meitav Dash, Excellence Nessuah and Altshuler

Shaham investment houses have kept their rank-

ing positions and are ranked second, third and

fourth. The Yelin Lapidot Investment House has

risen from sixth place to fifth place with a rise of

18% in its investment portfolio, stemming from

a rise in funds raised as well as a decline in re-

payments as well as a rise in values. For the first

time this year, alongside the investment house

rankings, a ranking table for portfolio manage-

ment companies is being presented (according

to the total of the portfolios managed in millions

of shekels).

Financial Services

300

60,000

55,000

250

50,000

45,000

200

40,000

35,000

150

30,000

25,000

100

20,000

15,000

50

10,000

5,000

0

0

2015

2014

2013

2012

2011

2010

2009

Number of Issuances Overall Volume of Raised Capital (in million NIS)

Source: Tel-Aviv Stock Exchange

100

304

160

109

283

Overall Volume of Raised Capital and Number of Issuances Multiyear

252

252

25

20

15

10

5

0

Oil

finance

Biomed

Technology

Industry

Insurance

Investments

Trade &

Services

Banks

Real Estate &

Construction

No. of Issuances in 2014 No. of Issuances in 2015

Source: Tel-Aviv Stock Exchange

Number of Issuances According to Sectors

27

2016

|

DUN’S

100

DUN’S

100

|

2016

DUN’S

100

|

2016

2016

|

DUN’S

100

Financial Services