8 / 730

8 / 730

I

n 2015, the most prominent factors in the

global economy were the geo-political

processes in China and in the Middle East.

China – the growth driver of the global economy

– has displayed a decline in its GDP growth rate

since 2010, mainly due to a trend of increasing

production costs in China and a decline in the

prices of commodities. The zero interest rate

policy led to a huge increase of global debts.

The world currently owes almost three times as

much as it produces, with the debt amounting to

c. $220 trillion. The main concern is that when

the interest rates will rise, several debt niches

would find it difficult to serve their debts, for

example the debts in China’s corporate and

household sectors. Since November 2014, the

central bank of China made 6 interest rate cuts

in order to increase consumption and invest-

ments and mainly in order to encourage China’s

middle class to transfer funds into the capital

markets, with the unstated goal being – to in-

crease the extent of raised bonds, in order to

enable Chinese companies to make extensive

investments around the globe. In the past three

years, we saw an increase in the contribution of

the developed countries to the global growth,

and a decline in the contribution of the devel-

oping countries to the global growth, mainly

because of China, which leads the developing

countries and currently produces c. 15% of the

global GDP.

The slowdown in China’s economic growth rate

and the surplus supply in Saudi Arabia’s oil pro-

duction led to a decline of commodity prices,

a matter which greatly affects the developing

countries, where there is a high share of com-

modities in the national income.

The Israeli economy

Israel’s economy is changing – and becoming

more commerce- and services-oriented and

less industrial. In 2015, the number of newly

opened businesses increased by c. 6%, a good

increase in comparison to stagnation in the

previous five years. However, the number of

closed businesses showed a similar increase,

so that the net increase was similar to its level

in the previous year. In 2016, we expect that

the number of newly opened businesses will

continue to increase and we estimate that it

would amount to 57,240 businesses.

We estimate that the number of closed busi-

nesses will show a sharper increase and would

amount to 48,861, so that the overall net in-

crease of businesses in this year will be 8,379

businesses, c. 12% less than in the previous

year. The main reason for the decline in the

net increase of businesses in 2016 is that the

current mix of businesses includes more busi-

nesses in the commerce sectors, which are

more risky in comparison to other sectors. So

it’s true that the number of newly opened busi-

nesses increased, but what type of businesses

were added to the economy? Mainly service

providers. The industrial and agricultural sec-

tors are fading, with a negative net increase

that continues the trend of the last three years.

Service providers constitute about 65% of the

businesses in the economy, but they only they

generate only c. 30% of the income and there-

fore we will not feel this increase significantly

in the GDP.

In 2015 the economy indeed recorded posi-

tive macro-economic data, an annual growth

rate of 2.5%. Nevertheless, the situation of the

businesses in this year deteriorated. The main

reason for this discrepancy was margin erosion

across almost every industry of the economy.

Businesses find it harder to achieve income

growth, to maintain profitability and to finance

their working capital needs. The margin ero-

sion, along with an increase in the leverage,

leads to an increase of the risk level. So that the

risk level of one third of the active businesses

increased during the last year. It is difficult to

develop a business when the managerial inputs

are dedicated to financing working capital and

debt collection. The trend of increasing average

collection period (“credit days”) continued in

2015, with an increase of c. 2.5% in the average

The Israeli and the global economies in 2015

And a forecast for 2016

10

8

6

4

2

0

-2

-4

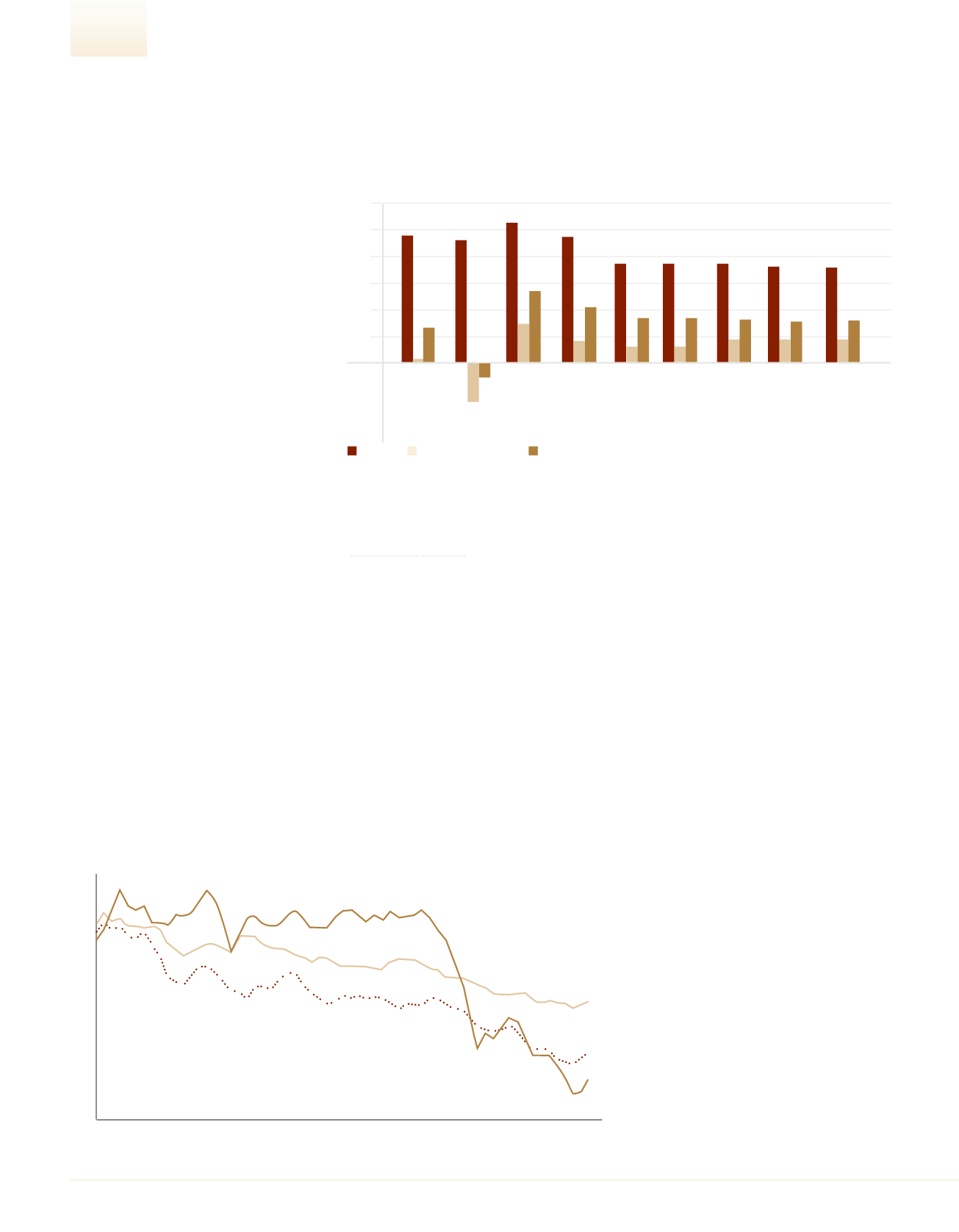

China Advanced Economics World

0.2

-3.1

-0.1

2012

2010

2013

2015

2011

2014

2016

9.2%

10.6%

9.5%

1.7%

1.2%

1.2%

1.8%

1.9%

1.9%

4.2%

7.7%

7.7%

7.7%

6.9%

6.5%

3.3%

3.1%

3.5%

3.3%

3.4%

3.1%

3.2%

5.2%

2009

9.6%

2008

China Convenes to a More Moderated Growth

The Decline in Commodity Prices Damages Growth Predictions

Jan 15

Jan 16

Mar 14

May 13

May 15

May 16

Jul 12

Sep 11

Nov 14

Jan 14

Mar 13

Mar 15

Mar 16

May 12

Jul 11

Sep 14

Nov 13

Nov 15

Nov 16

Jan 13

Mar 12

May 11

Jul 14

Sep 13

Sep 15

Sep 16

Nov 12

Jan 12

Mar 11

May 14

Jul 13

Jul 15

Jul 16

Sep 12

Nov 11

Jan 11

US% indexes, 100=2010

150

130

110

90

70

50

30

8

2016

|

DUN’S

100

DUN’S

100

|

2016

DUN’S

100

|

2016

2016

|

DUN’S

100