116 / 730

116 / 730

T

he rapid growth in demand against the

restricted supply is expected to con-

tinue and enhance the rise in housing

prices in Israel, in the coming years. The annual

rate of housing price rises sped up in the sum-

mer of 2015 to about 5.6%, compared to the

average 4% at the beginning of the year. Sales

of new apartments in the 12 months that ended

in October 2015 were 35%higher compared with

the previous 12 months and reached more than

30,000 housing units.

1

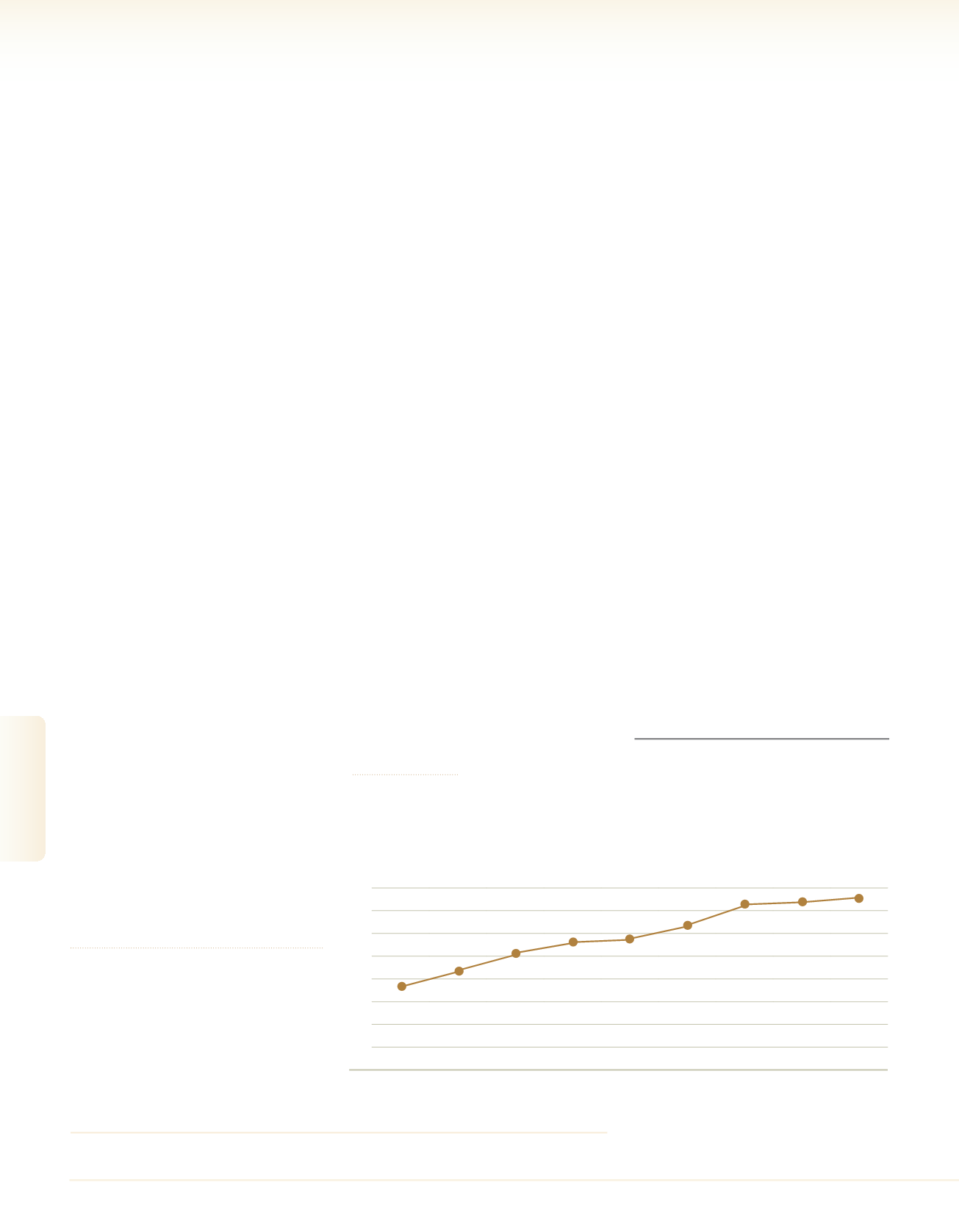

In this graph it is possible to see the steep in-

crease in housing prices in the past few years,

which characterizes the field of residential real

estate.

The situation of the housingmarket is dependent,

among other things, on the success of various

government plans. The new "Buyers Price Target

Plan" (Mechir Lamishtaken) (a plan that offers

apartments at discounted prices for those en-

titled), significantly expanded the groups entitled

to participate in the plan and those entitled to

participate can now do so without meeting sal-

ary threshold conditions/military service/ family

status, etc. In addition, the new plan does not

restrict the size of apartments, provides a grant

of between NIS 40,000 and 60,000 in outlying

regions, and subsidizes land development, by

more than 40%.

Choosing participants from among those with

entitlement who registered for the project is

conducted through a lottery, carried out by the

Ministry of Construction and Housing. Those in-

terested in registering for the lotterymust submit

an application to theMinistry of Construction and

Housing to receive a certificate of entitlement

via the Mechir Lamishtaken website. Purchas-

ing these apartments is restricted to first time

homebuyers or someone who has not owned a

home in recent years.

Building Starts and Building Finishes in 2015

In 2015, construction began on about 47,750

new homes in Israel's economy, of which about

27%were in buildings with one or two units (de-

tached and semi-detached houses). The number

of homes began during this period was 3.9%

higher compared with the corresponding period

of 2014.

The largest number of homes on which con-

struction was begun in 2015 was recorded in

the Central District and represented about 25%

of overall homes, while in the JerusalemDistrict,

there were only about 10% of total homes.

In 2015, compared with the corresponding period

of 2014, a rise of about 48% was recorded in the

Southern District, about 8% in the Tel Aviv Dis-

trict, about 7% in the Northern District and about

1% in the Jerusalem District. In contrast, over the

same period there was a decline of about 11%

in the Central District and about 8% in the Haifa

District.

About 54% of the homes on which construction

began in the Northern Region were detached or

semi-detached houses, compared with 6% in the

Tel Aviv District.

During the year construction of about 43,400

homes was completed, about 2.8% less than the

corresponding period of 2014. About 30% of the

homes built were in detached or semi-detached

houses.

The largest number of homes completed was in

the Central Region – about 29% of the overall

homes were in that region, while in each of the

Haifa and Jerusalem Regions this figure was only

about 10%.

There was a decline of about 17% recorded in the

Southern District and of about 10% in the Haifa

District compared with the corresponding period

in 2014. In contrast, there was a rise recorded of

about 15% in the number of homes in which con-

struction was completed in the Tel Aviv District.

2

Sheltered Housing

There is a close connection between the scale of

activities in sheltered housing in Israel and the

constant increase in the Israeli population, the

rise in the standard of living, and the rise in life

expectancy of the Israeli population. According to

estimates in this sector, there are about 12,500

sheltered housing unitswithmost of themconcen-

trated in the Tel Aviv Metropolitan and Hasharon

regions. In many of the sheltered housing homes

tenants have a range of services including swim-

ming pools, spas, fitness rooms, extra-curricular

activities, restaurants, clinics, etc.

The companies operating in this sector are faced

with hardships in expanding due to the relatively

low supply of available land in Israel for sheltered

housing complexes, whichmoderates the compe-

tition in the sector and mainly allows expansion

of operations through the purchasing of existing

homes from other companies.

Themostdramaticchangeinthefield,whichmight,

among other things, influence future rankings, is

the entry of the Azrieli Group into the sheltered

housing sector. During 2015, the Group acquired

the Palace sheltered housing home in Tel Aviv,

which is considered one of the most luxurious in

the country. As this article is being written, the

Azrieli Group is working towards acquiring Ahuzat

Bayit, Ra'anana, which will join the two projects

that the Group is developing in the sheltered hous-

ing sector in Modi'in and Lahavim, and which are

planned to be occupied in 2018.

Construction & Real Estate

Average Housing Price Index

385.6

365.9

359.2

400

326.4

350

299.3

289.9

300

262.3

223.0

250

196.2

200

150

100

50

0

Until May

2016

2015

2014

2013

2012

2011

2010

2009

2008

Source: Central Bureau of Statistics

1

The Israeli Housing Market, December 2015 Stan-

dard & Poor's Maalot.

2

Building starts and building finishes, 2015, Central

Bureau of Statistics.

116

2016

|

DUN’S

100

DUN’S

100

|

2016

DUN’S

100

|

2016

2016

|

DUN’S

100

Construction & Real Estate